Policy Behind AI and Blockchain

AI and Blockchain on Business Policy and Law

Two progressive technologies have dominated the modern computing era: blockchain technology and artificial intelligence. AI devices perform tasks that require seemingly high intelligence, while a blockchain is a decentralized log that stores data in highly encrypted format. With the rapid growth of computing technology, there’s the need to integrate these two into business policy and law. The integration process entails practices that make it easy to regulate unknown technologies. These technologies also come with unforeseen circumstances in both the social and corporate environment. There is the need to create policies and procedures that can anticipate and address these circumstances.

Further, some late adopters have put up a resistance against the adoption of these technologies. The adoption policies need to address this resistance. Finally, adoption into business policy and law should address the role that each technology is going to play. So far, blockchain technology has revolutionized the internet, for storing and encrypting information while keeping it decentralized (Vreeswijk, 2003). Artificial intelligence, while still in its formative stages, has enabled computers to perform human-like tasks using information stored in databases. Integrating Blockchains and AI would mean these two technologies complement each other, enabling great strides in business, technology, and governance among other areas. AI technologies shall, therefore, find use in improving business efficiency while blockchain technology will be used for smart contracts and transactions.

Principles Behind AI in Business Policy and Law

AI technology will change the way we conduct business and administrative activities. While advances in technology promise efficient machines that reduce the workload on humans, they introduce policy issues since they are economic disruptors. One of the largest concerns is the loss of jobs owing to replacement (Cunningham, 2004). The technology only promises to help improve human efficiency, not to eliminate the need for workers. So far, engineers have successfully integrated AI into process automation. Process automation tasks include email and phone record operations, handling customer communications, and using natural language processing to extract provisions from legal and contractual documents.

AI has also been used in business for its cognitive insight. Machine Learning algorithms help detect patterns and identify meaning in vast volumes of data. This functionality has found application in such areas as market prediction, identity theft/credit card fraud, and identification of safety issues in products that are brought in for warranty, automation of targeted advertisements and precise actuarial modeling (Cunningham, 2004). Machine learning and its associated technologies (such as deep learning) can identify patterns in speech and images with nearly the same cognitive ability of humans.

Cognitive engagement is the third application of AI in business and administration. Cognitive engagement communicates with personnel and staff using natural language processing techniques (Payr, 2011). These techniques encompass chatbots, intelligent agents, and machine learning. Applications of cognitive engagement in modern business include: customer service & technical support, internal applications for employee feedback, goods and services recommendations systems and medical recommendation systems. Companies have reported tremendous success using cognitive engagement for both staff and clients.

FIGURE 01: Boston Consulting Group & MIT Sloan Management Review, Reshaping Business With Artificial Intelligence (Forbes, 2017).

Principles Behind Blockchain Smart Contract Technologies in Policy and Law

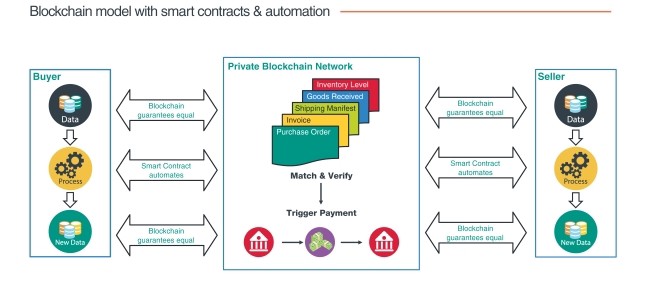

Blockchain technology has evolved beyond the decentralized transaction system it was at its onset. Cryptocontracts, popularly known as smart contracts, are a popular example of evolved blockchain technology evolution. Smart contracts enable the transfer of digital assets under specific conditions. These contracts allow trading parties to enter legal contracts via a peer-to-peer arrangement (Bhandari, 2018). Blockchain technology writes the term of contract into the lines of code. No single person is in charge of the transaction, and this eliminates third-party transaction fees. With a shared record of transactional history and the contractual agreement between the parties, smart contracts are finding application in various professional fields.

In healthcare, smart contracts have led to improved patient privacy, enhanced information sharing, and processing of bills and insurance (Cyran, 2018). In real estate, the technology could be used for financing, funding, and management of lease agreements. Blockchain technology is, therefore well suited to handle business activities. The contracts can help businesses streamline procedures, protocols and processing of transactions.

FIGURE 02: Blockchain Smart Contract Model Diagram (Codeburst, 2017).

AI can be used to improve logistics processes so that companies can respond to dynamic market shifts. The technology offers viable solutions to predict demand patterns, determine loading schedules, and choosing the best product distribution routes (Cyran, 2018). This technology, therefore, helps employees who constantly face issues related to scheduling, transport costs, staff management and so on.

This offloading comes at a cost. Most people face the prospects of losing their jobs to AI machines. Proponents of AI argue that this is not a valid concern, given the technology is only aimed at automating the workload and eliminating non-value added activities. AI technologies are made to prime the way employees perform. There are too many nuanced interactions and judgments to be made in a workday that a software algorithm cannot handle (Cunningham, 2004). Technologists should, however, exercise care when developing adoption plan for these technologies, as they could face resistance owing to the job loss argument.

These technologies are economic disruptors, changing the way we handle global business. They have transformed every aspect of industry, from production, prototyping to securing financial transactions. AI and blockchain technology redefine human roles in business by reducing the workload and eliminating non-value based business (Bhandari, 2018). By adopting these technologies, humans can focus on productive, creative activities that lead to societal and individual growth.

These technologies also stem off from Level 2 technologies that are currently widespread. Recent advancements in computing have put AI and blockchains at the center of most industrial and business processes (Vreeswijk, 2003). These technologies have been integrated into organizational systems, and are slowly taking up more of the capabilities formerly reserved for Level 2 technologies. Some early adopters of level 2 technologies who are yet to embrace the impact of AI and Blockchains put up resistance, citing such reasons as economic turmoil and job loss to support their apathy.

Policy should help in the implementation of an adoption program for any new technologies. AI and blockchain technology have found increasingly larger applications in modern industry and business processes. Proper policies and procedures shall allow the adoption of these technologies without the unforeseen circumstances of economic turmoil and job loss. Proper adoption could see AI improve efficiency in business processes while reducing the workload on human labor. Blockchain technology shall help in the implementation of smart contracts which shall improve reliability and security in financial transactions.

- Allenby, B., & Sarewitz, D. (2011). The Techno-Human Condition. The MIT Press Cambridge, 49(02). ISBN-13: 978-0262525251

- Bhandari, B. (2018). Supply Chain Management, Blockchains and Smart Contracts. SSRN Electronic Journal. Doi: 10.2139/ssrn.3204297

- Chandrayan, P. (2017, August 30). Blockchain Technology Part 2 : Smart Contract Fundamentals. Retrieved from https://codeburst.io/blockchain-technology-part-2-smart-contract-fundamentals-d243e2311f94

- Columbus, L. (2017, September 12). How Artificial Intelligence Is Revolutionizing Business In 2017. Retrieved from https://www.forbes.com/sites/louiscolumbus/2017/09/10/how-artificial-intelligence-is-revolutionizing-business-in-2017/#3fc3fe5463a3

- Cunningham, P. (2004). Introduction: The 14th Artificial Intelligence and Cognitive Science Conference (AICS-03). Artificial Intelligence Review, 21(3/4), 191-192. Doi: 10.1023/b:aire.0000036254.44436.14

- Cyran, M. (2018). Blockchain as a Foundation for Sharing Healthcare Data. Blockchain in Healthcare Today. doi: 10.30953/bhty.v1.13

- Payr, S. (2011). SOCIAL ENGAGEMENT WITH ROBOTS AND AGENTS: INTRODUCTION. Applied Artificial Intelligence, 25(6), 441-444. Doi: 10.1080/08839514.2011.586616

- Vreeswijk, G. (2003). Book Review: Bayesian Artificial Intelligence. Artificial Intelligence and Law, 11(4), 289-298. Doi: 10.1023/b:arti.0000045970.25670.25

Sponsor

Peter W. Ross, Ph.D. CUNY

Philosophy of Mind, Cognitive Science

Leave A Comment